The Collapse of Silicon Valley Bank (SVB)

The Collapse of Silicon Valley Bank (SVB)

March 13, 2023 | By Professor Alan Moreira

Founded in Santa Clara, California, in 1983, Silicon Valley Bank (SVB) provided financing for nearly half of U.S. venture-banked technology and healthcare companies. Its spectacular collapse on March 10 marks the second-largest bank failure in U.S. history. The next day, Signature Bank followed suit in the third-largest bank failure in U.S. history.

As startups scramble to recoup their deposits and policymakers leap into action to quell fears of financial contagion, the rest of us are assembled around the smoldering ruins of SVB, working to piece together what happened.

What we know.

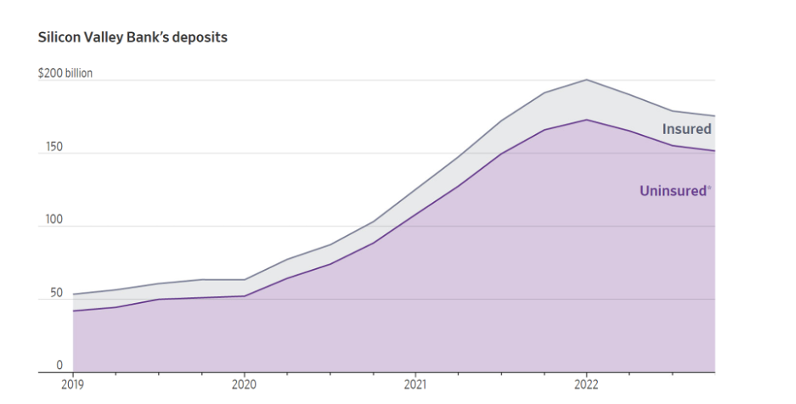

SVB grew quickly by taking unusually large deposits. In fact, the vast majority of its funding was in uninsured deposits. At the peak of its size, only $25 billion of SVB’s $200 billion worth of deposits were insured. This means the bulk of its funding was labeled “deposits” but had the properties of much less stable wholesale funding—funding that dries up extremely quickly at the first sign of trouble. (For an example of this phenomenon, you can reference The Macroeconomics of Shadow Banking, which I co-authored with Alexi Savov).

SVB had a liability side that resembled a money market fund, which tends to hold very short-term maturity assets. In reality, though, it operated more like retail-oriented banks such as Bank of America and Wells Fargo in that it held assets of fairly long duration. This turned out to be a fatal error because SVB was not like most retail-oriented banks. Case in point: one of SVB’s depositors was famously beleaguered stablecoin USDC, which had parked $3.3 billion in deposits in the bank. Put simply, an account with that much money does not behave like small retail deposit accounts.

In general, retail depositors are much less responsive to the news—and much less responsive to changing interest rates. So for banks like Bank of America and Wells Fargo, who have “sleepy depositors,” it does make sense to own fairly long duration assets (See Banking on Deposits: Maturity Transformation without Interest Rate Risk by Itamar Dreschler, Alexi Savov, and Philipp Schnabl for further discussion). While we can debate the extent to which this stability of retail deposits is really a structural and invariant property of the financial system, what is not debatable is that wholesale funding—which constituted the bulk of SVB’s funding—is fickle and responds quickly to all sorts of news. We learned this the hard way during the financial crisis.

With this deep mismatch in the duration of SVB’s assets and liabilities, the rapid pace of interest hikes generated a precipitous drop in the market value of its assets. This was the case for every other U.S. bank as well. Historically, it has worked out for them because retail depositors stick around. Normally, the hold to maturity value of the assets, which is not impacted by changes in interest rates, is the right metric to gauge the value of a bank and its assets.

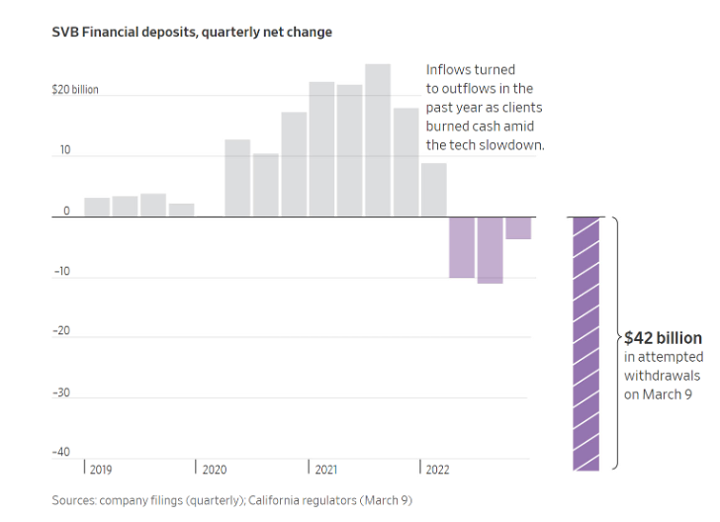

Unfortunately for SVB, things did not go according to the typical script. Leading up to its failure, it had been experiencing outflows of roughly 5% of its deposits per quarter. This means that in the last nine months alone, it realized losses on about 15% of its portfolio.

Then came the full-fledged run on the bank. To the best of my knowledge, this run was sparked by SVB’s March 9 announcement that in order to fund the higher-than-expected deposit outflow, it had realized losses of nearly $2 billion. The announcement triggered a frenzy of attempted withdrawals on approximately $42 billion the next day. The Federal Deposit Insurance Corporation (FDIC) quickly swooped in to take over the bank.

What we don’t know.

We still don’t know if SVB has incurred other losses associated with the riskier side of its balance sheet. As SVB was the go-to bank of Silicon Valley in a time when tech stock was already taking a beating, it wouldn’t be surprising to learn that it had plenty of other bad loans on its books. We don’t know this for sure, but we might infer something about the quality of the bank’s lending practices from the fact that it was already experiencing abnormally high outflows prior to its March 9 announcement. Perhaps its depositors knew that SVB was being overly aggressive with its lending practices. Sometimes a deal that seems too good to be true can backfire, pushing away would-be customers.

When the FDIC takes over a bank, its mandate is to protect the insured depositors. It can accomplish this aim by selling the entire bank to a competing banking (which happened frequently during the 2008 crisis), or it can choose to liquidate the bank’s assets to honor the insured depositors. On one hand, the FDIC has the flexibility to minimize its own costs by avoiding liquidation. On the other hand, policymakers are clearly worried that the fall of SVB might create a ripple effect, sending the banking industry hurtling toward financial chaos similar to the 2008 crisis.

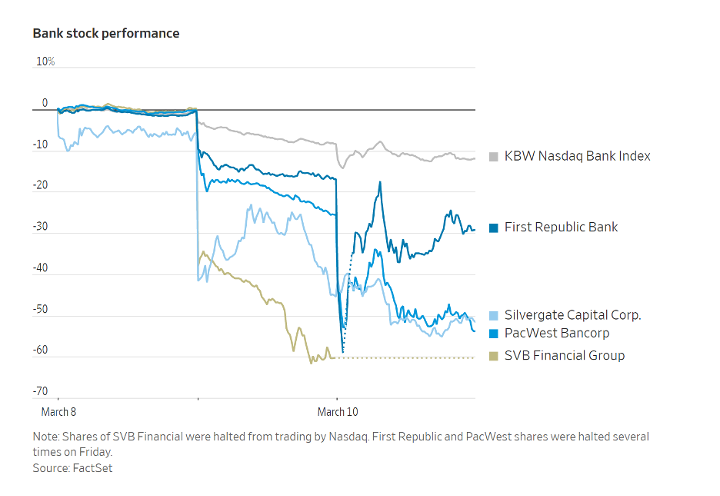

We already see that the woes of SVB seem to be spreading to other banks.

To prevent a domino effect, the FDIC joined the U.S. Department of the Treasury and the Federal Reserve in announcing it would guarantee all deposits in the SVB, not just deposits up to the standard limit of $250,000. This takes us back to the policy in place from early 2009 to 2012, the last time the limit was lifted, but only for SVB and Signature Bank, which failed in the same weekend.

It is easy to grasp why policymakers have chosen this path. By ensuring all deposits of SVB, they are hoping to reassure the rest of depositors in the financial system that their deposits are safe. Their aim is to avoid a replay of the devastating, slow-moving chaos that seeped through the banking industry from the summer of 2008 to the spring of 2009.

But as of March 13, policymakers have yet to announce a formal policy that all depositors in the financial system are insured. This is a misstep that represents the worst of two worlds. They used assets derived from the rest of financial system to bail out wealthy Silicon Valley venture capitalists, but to this point have done little to reassure depositors in other banks, which is critical for financial stability.

This pattern of policy through promises is nothing new. It has been the hallmark of central banker interventions in the last two decades. (See Whatever It Takes? The Impact of Conditional Policy Promises, my recent working paper with Valentin Haddad and Tyler Muir).

My greatest concern is that we are about to replay one of the worst features of the 2007-2009 crisis. In those years, policymakers intervened strongly to rescue some companies but not others. For example, the Fed was highly aggressive in helping JP Morgan swallow up Bear Sterns. Then, when Lehman Brothers was floundering a few months later, policymakers claimed they had no mandate to act. Looking back, it is clear they thought that by being forceful in specific cases, they could lead the market to expect stronger interventions in the future even though those interventions did not come to pass. After a considerable amount of chaos, they ended up taking the necessary action to introduce a system-wide guarantee to deposits.

These implicit promises are being tested again but now at much faster speeds.

The bottom line.

The core issue at hand is that SVB’s liability was mostly DINOS—deposits in name only. One key lesson to take away from the crisis is that policymakers should regulate financial entities based on their behavior, not their description. SVB was, in essence, an undiversified shadow bank that was funded almost completely with wholesale funding but was stuffed with long-term assets. It was a disaster waiting to happen. Now, it remains to be seen whether federal action to prevent a cascade of failures will have its intended effect.

Alan Moreira is an Associate Professor of Finance at the Simon Business School.

Alan Moreira is an associate professor of finance at the Simon School of Business.

Follow the Dean’s Corner blog for more expert commentary on timely topics in business, economics, policy, and management education. To view other blogs in this series, visit the Dean's Corner Main Page.

Related Blogs

-

AGI could emerge within decades, bringing risks like job loss, misuse, misalignment, and even consciousness. Are we ready? Prof. Huaxia Rui explores the stakes.

AGI could emerge within decades, bringing risks like job loss, misuse, misalignment, and even consciousness. Are we ready? Prof. Huaxia Rui explores the stakes. -

The new Department of Government Efficiency (DOGE) sparks debate. Is it streamlining bureaucracy or pushing privatization? Joseph Kalmenovitz unpacks its impact in this Q&A.

The new Department of Government Efficiency (DOGE) sparks debate. Is it streamlining bureaucracy or pushing privatization? Joseph Kalmenovitz unpacks its impact in this Q&A. -

Understanding Creditor Rights and Their Impact February, 26 2025 | By Giulio Trigilia Creditor rights are often seen as a key driver of investment and economic growth, but research suggests the reality is more complex. While stronger protections can improve borrowing conditions in competitive

Understanding Creditor Rights and Their Impact February, 26 2025 | By Giulio Trigilia Creditor rights are often seen as a key driver of investment and economic growth, but research suggests the reality is more complex. While stronger protections can improve borrowing conditions in competitive -

Online steering shapes how we shop, but is it fair? Simon professors Andras Miklos & Jeanine Miklos-Thal explore its ethical and economic impact in a new paper.

Online steering shapes how we shop, but is it fair? Simon professors Andras Miklos & Jeanine Miklos-Thal explore its ethical and economic impact in a new paper. -

AI regulation must balance innovation and fairness. A recent keynote at Simon explored how competition and antitrust shape the evolving AI landscape.

AI regulation must balance innovation and fairness. A recent keynote at Simon explored how competition and antitrust shape the evolving AI landscape. -

In this blog, Simon alumnus Josh Goldberg explains the 25-year journey of model risk management.

In this blog, Simon alumnus Josh Goldberg explains the 25-year journey of model risk management. -

In this blog, Dean Sevin Yeltekin points to productivity as the key ingredient that drives US economic growth.

In this blog, Dean Sevin Yeltekin points to productivity as the key ingredient that drives US economic growth. -

ChatGPT as a Marketing Assistant October 16 | By Professor Professor Paul Ellickson In this blog post, Professor Paul Ellickson describes the potential of machine learning and Generative AI tools to predict and improve the performance of marketing campaigns. Identifying and optimizing targeted

ChatGPT as a Marketing Assistant October 16 | By Professor Professor Paul Ellickson In this blog post, Professor Paul Ellickson describes the potential of machine learning and Generative AI tools to predict and improve the performance of marketing campaigns. Identifying and optimizing targeted -

In this blog, Professor Alan Moreira unpacks the effects of policy promises on financial markets.

In this blog, Professor Alan Moreira unpacks the effects of policy promises on financial markets. -

Professor Narayana Kocherlakota points to real wage decline to explain widespread voter pessimism about the U.S. economy.

Professor Narayana Kocherlakota points to real wage decline to explain widespread voter pessimism about the U.S. economy. -

In this blog, Dean Sevin Yeltekin and Simon summer intern Defne Olgun take a closer look at the mismatch between economic indicators and voter perception.

In this blog, Dean Sevin Yeltekin and Simon summer intern Defne Olgun take a closer look at the mismatch between economic indicators and voter perception. -

Partisan Regulatory Actions July 3 | By Vivek Pandey Professor Vivek Pandey presents evidence that the SEC treats firms differently based on political ideology. It’s no secret that Americans are more politically divided than ever. Intense political polarization has crept into every corner of society

Partisan Regulatory Actions July 3 | By Vivek Pandey Professor Vivek Pandey presents evidence that the SEC treats firms differently based on political ideology. It’s no secret that Americans are more politically divided than ever. Intense political polarization has crept into every corner of society